The Federal Open Market Committee of the Federal Reserve (Fed) meets tomorrow and Wednesday to determine interest rates. Given recent economic news, most analysts expect the Fed to cut interest rates.

The Fed has a dual mandate to ensure stable prices and maximum employment. In this respect, it is different than many other central banks, who are generally only tasked with keeping inflation low. To make the Fed’s task more difficult, they only have one tool, interest rates, to accomplish these dual goals. When you hold a hammer, everything looks like a nail.

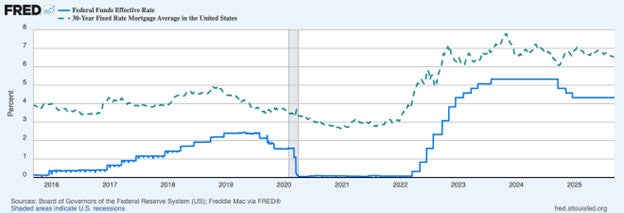

Moreover, the Fed only controls one specific interest rate, the federal funds rate (FFR). This is the interest rate that commercial banks lend to each other overnight to meet their reserve requirements. The current FFR is 4.3%, with the last cut in December 2024. Other interest rates, that consumers care more about, tend to move in line with the FFR, but not always. The graph below shows this correlation, but although the Fed raised the FFR in 2016, the 30-year mortgage rate fell.

Given the dual mandate, if the Fed is more concerned about rising prices and inflation, then it would raise interest rates to curtain consumer spending and firms’ investments. If, on the other hand, the Fed is more concerned with labor market weakness, it would cut interest rates.

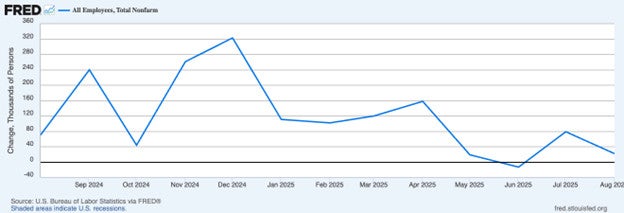

Recent economic data has the Fed more concerned about the labor market than inflation. The national economy only added 22,000 jobs in August and lost jobs in June. There are now more unemployed persons (7,384,000) in the U.S. than than are job openings (7,181,000) for the first time since the spring of 2021.

On the other hand, inflation remains stubbornly above the Fed’s target rate of 2%. The August Consumer Price Index measure of inflation came in at 2.9% and has risen from 2.3% in April. The Fed’s preferred measure of inflation is the Personal Consumption Expenditures price index because it is broader-based and it increased by 2.6% in July, up from 2.2% in April. There is some evidence that tariff rates are impacting overall prices, although firms are not passing all the higher taxes onto consumers.

Mild stagflation (a stagnating labor market accompanied by inflation) leaves the Fed between a rock and a hard place. Maintaining the current interest rate will help curtail the recent run-up in inflation but harm the labor market. Alternatively, lower interest rates will help the weak labor market but stoke inflation. The bigger threat right now seems to be the weak labor market, and I expect, as most people do, the Fed to cut interest rates at the end of its meeting tomorrow. I suspect that by just 0.25 percentage points thought there is the possibility of a 0.5 percentage point cut.