After a year of soaring inflation, the IRS has raised the dollar amounts needed to qualify in each tax bracket for 2023, along with increases in standard deductions and other areas.

The IRS has seven tax rates based on income levels – 10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent, and 37 percent.

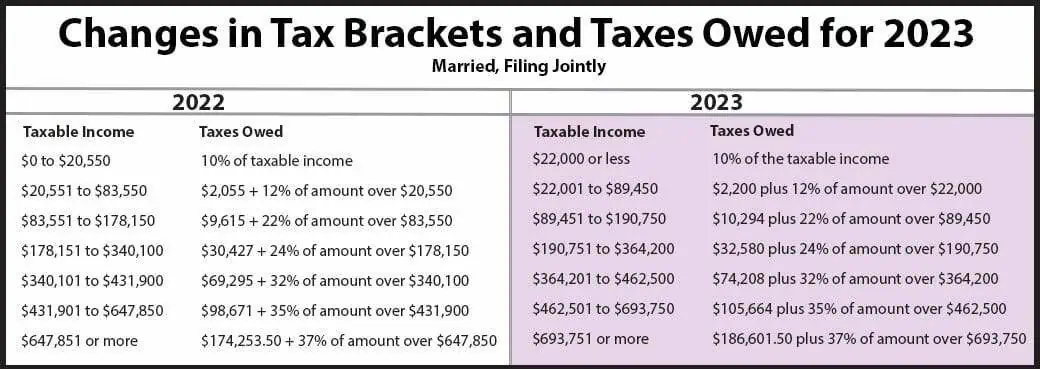

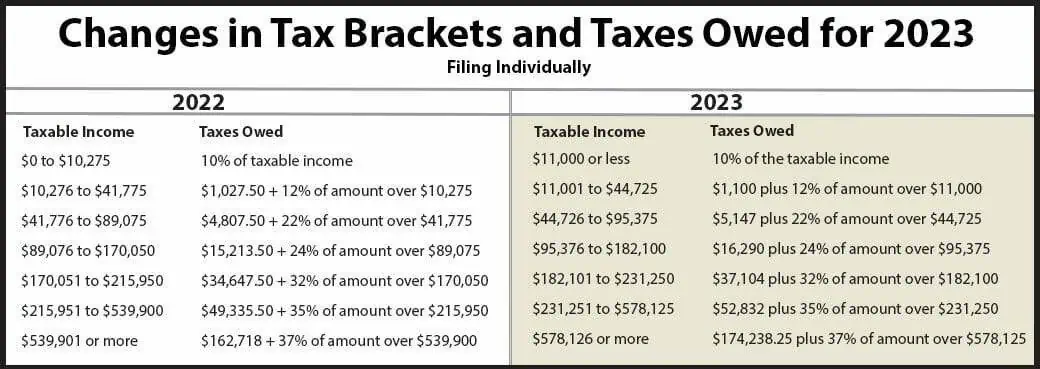

The rates for 2023 have remained the same but the amounts needed to qualify for each bracket have increased. For example, in 2022, the 22 percent bracket for those married and filing jointly was $83,551 to $178,150; for 2023, that bracket will be for those earning $89,451 to $190,750.

However, except for the lowest bracket, the percentage of the tax rate is not applied to your entire income. It is an accumulation of the rates along the way. For example, if a married couple filing jointly earned $100,000, they would pay 10 percent on the first $22,000 ($2,200) and 12 percent on the amount between $22,001 and $89,450 ($8,094) and then 22 percent on the remainder ($2,321).

But there is a chance some people might save a bit of money, since the standard deductions have also been increased; for married filing jointly, it moved from $25,900 to $27,700 and from $12,950 to $13,850 for individuals.

There are also other increases for 2023 in IRA and HSA contributions. There are also many other changes that will affect the taxes you pay next April. Consulting a local CPA or tax attorney now can help you make the most of any changes, so you won’t be left scrambling at the end of the year.