Trying to buy a house in the market we are in can be very discouraging to new home buyers in the $150,000 to $250,000 price range. I have a current client, who is a good friend of mine, and he has been looking to buy his first house for a few months now.

There were weeks when we would view a newly listed home every single day. We made plenty of offers – I think our score count was 0 offers accepted and 10 offers made, so we were 0-10.

As his realtor and friend, I could see the growing disappointment with every rejected offer. He has a great job, not a lot of debt, and was approved for a solid conventional loan. We were making very aggressive offers; i.e., offering at least 10 percent over the listing price, asking $0 in closing costs, and providing 3-5 percent earnest money.

Eventually, we started to remove any due diligence period and just asked for the right to negotiate repairs. Even still we were getting beat out by people who could offer all cash or had the extra cash to pay any appraisal difference.

The losses were starting to take their toll so much, so he was ready to end his search and overpay to rent somewhere.

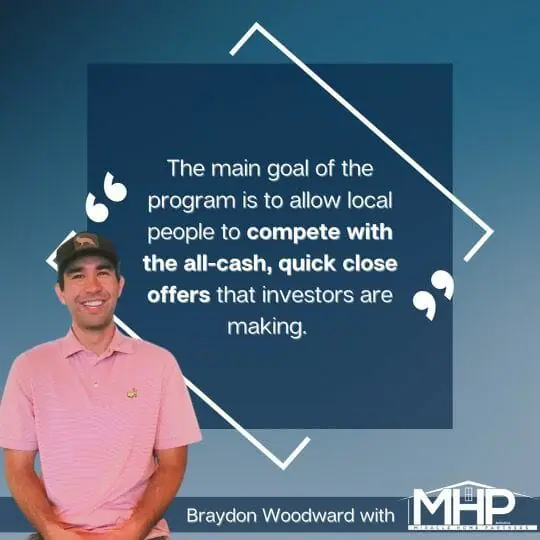

It was at this point, that a mortgage officer I work with contacted me and told me about a new program the mortgage company had just started, called the Buyers Accepted Program. It allowed their clients to make 100 percent cash offers after being approved for the program. The main goal of the program is to allow local people to compete with the all-cash, quick close offers that investors were making.

After learning about this new program, I hopped on a zoom call with 30 other realtors to learn more about Buyers Accepted and how to get certified to work with this loan.

Essentially, the mortgage company will complete a full underwriting review of the buyer’s account before being accepted into the program. Once the buyer is approved, they can start making cash offers in the name of Buyers Accepted, LLC. Buyers Accepted will then put their cash upfront to purchase the property (this allows for a quick close on the seller’s side).

After an offer has been accepted, there will be a contract between Buyers Accepted and the end buyer, which will work out like any other conventional loan.

Once the first closing takes place, Buyers Accepted allows the buyer to move into the property before closing the second contract. They do require rent to be paid, but it is typically just a couple of weeks until the final closing.

You’re probably thinking, “what’s the catch?” Everyone wants to know about the fees for this program and to be honest, it’s a pretty good deal. They charge a 1.5 percent fee and will invoice you any costs they accrue from the first closing.

If you are not seeing much success with your traditional loans, I highly suggest asking your mortgage company if they have any other creative ways to make your offers stronger.

If you have any questions about the Buyers Accepted program, or how to get started with it just give us a call.

P.S. My client from above has finally got an offer accepted. We are 1-for-3 after making Buyer Accepted offers!