At a Federal Reserve meeting held on Wednesday, June 15, officials agreed to another 0.75 percent raise to their interest rate. The news was not what anyone in the mortgage industry was hoping to hear. It is scary to imagine that this is just the beginning.

The Wall Street Journal noted that we could see an additional 1.75 percent added by the end of this year. They also noted that at this pace of increase, we would see the most aggressive rate rise cycle since the 1980s.

In 1983, the average 30-year mortgage rate was 13.24 percent. I am not an economist, financial planner, money guru, or qualified in any way to predict what will happen next, but common sense tells me that we are about to see some very creative financing in the future. I know that shelter is one of our necessities, and as Americans, we are very accustomed to finding a way to have what we need. Shelter or housing is always going to be what we spend the largest chunk of our paycheck on.

We all need a place to live, and finding a way to make that work will continue to drive the real estate and mortgage marketplace. I want to share some information on what an adjustable-rate mortgage is. They have notoriously been deemed as bad mortgage options or high risk for good reason, but they will have a prominent place in the future, as they did in the past.

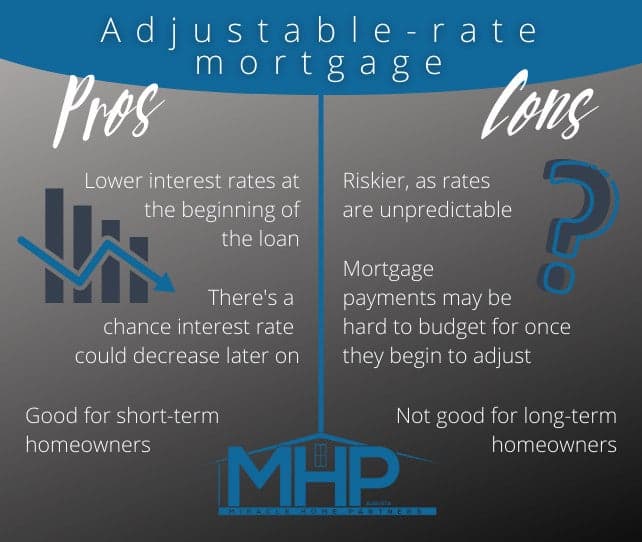

First, adjustable-rate mortgages, or ARMs, generally start at a lower interest rate than fixed-rate mortgages, so they should provide the lowest possible rate. They will start with a “fixed” rate period (usually 5, 7, or 10 years) and then “adjust” based on the terms you agree to.

The “adjustable” terms could max out at a previously determined rate, or fluctuate with the market. This is why they get a bad reputation. In the past, banks failed to clearly disclose the terms and risks, leaving the consumer confused and feeling like they were taken advantage of.

As a consumer, please remember that nothing is free, and someone somewhere is making money off lending money to you. Our need for housing is exploited by the governments and banks; that is how they make money. It is an unavoidable part of life unless you have the physical cash available to buy what you need.

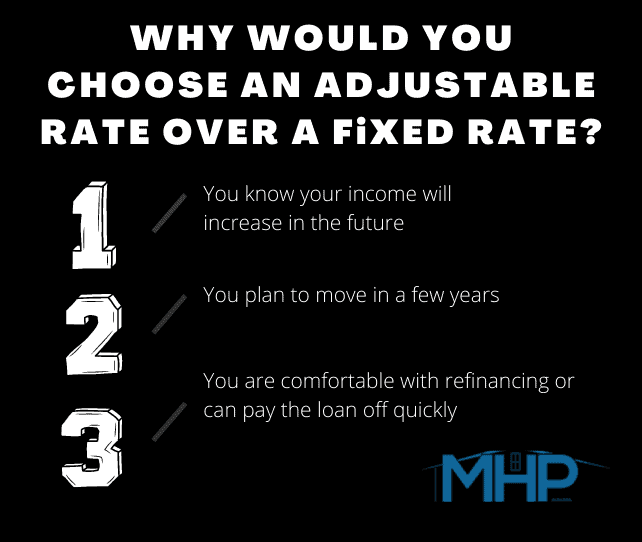

Who would be a good fit for an ARM? If you know you are not staying in a home more than the “fixed” rate term, this could be a good option for you. Or if you know you don’t want to move again, and at the end of your “fixed” rate term you will have a significant increase in income to cover the increased mortgage payment, this could be a good loan for you. If you make a ton of money and can pay the loan off in 5-10 years, this could be a good loan for you.

The scenarios are endless as to if you could benefit from this loan option.

If you are interested in more details to see if this would benefit your situation, I highly recommend you speak to a local mortgage specialist to find out what is best for you personally.